My Repayment Plan

Grrr… Outrageous loan payments:

It was one of the hottest days ever experienced in my life. In fact, according to the National Oceanic and Atmospheric Administration Summer, 2011 was officially the hottest ever for Texas. Sweat rolled down my forehead, over the bridge of my nose, and onto my laptop as I reviewed projected monthly loan payments. My apartment’s a/c unit and ceiling fans were all cranked full blast to no avail, my living room was an oven. I stared at the number slated to be my undoing and it stared back at me: $981.73, was my projected monthly payment. Then something happened…

My wife showed her support:

In frustration, I swung my fists angrily in the air and exclaimed through tears, “I have ruined myself financially!” To this my wife replied, “Boy, you are so dramatic” and let out a hearty laugh. At this point, there were two things in the world I did not particularly care much for: her and those blasted loans. She walked over to me said with a smile and said, “Your loans are my loans”.

Unlike me, my wife has $0 debt. She is currently in her graduate program and owes loan companies and the federal government nothing, I am very proud of her. Her educational background is also in sciences (Biology and Chemistry), she’s been blessed to have scholarships.

How I’ve tackled repayment:

I soon researched different repayment options through my loan servicers and applied for the Income-Based Repayment (IBR) program. In 2011, the maximum payment was 10% of your discretionary income; presently, it is 15%.

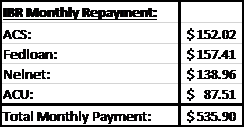

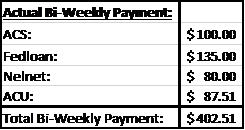

Below are tables displaying my monthly payments under IBR with each loan company. The first table below shows the initial monthly payment of $535.90 calculated for repayment. However, I decided to be more aggressive and pay $402.51 bi-weekly, bringing my monthly total to $805.02.

Less interest accrues on the principal loan balances with bi-weekly payments as opposed to monthly payments. This is because there is less time for interest to accumulate. This is a well known method used for paying mortgages, so I thought to myself, “Why not use this method when I have the mortgage without the house?” lol

Remember, my initial monthly payment was forecasted at $981.73, with complete repayment scheduled after 10 years.  Since I’m currently paying a total of $805.02, one would assume I’d end up behind on the “standard” 10-year schedule for repayment. But God blesses me throughout the year to make additional payments whenever possible. My current progress still slates me to be completed before the 10 year mark.

Since I’m currently paying a total of $805.02, one would assume I’d end up behind on the “standard” 10-year schedule for repayment. But God blesses me throughout the year to make additional payments whenever possible. My current progress still slates me to be completed before the 10 year mark.

So this is my repayment plan. The next blog entry will discuss my wife’s favorite… our personal budget. So I have questions to ask you. Are you currently taking advantage or ever even heard of the IBR program? Have you found creative ways to speed up your repayment process?

Hi there, just became aware of your blog through Google,

and found that it is truly informative. I am going to watch out for brussels.

I’ll appreciate if you continue this in future. Lots of people will

be benefited from your writing. Cheers!

LikeLike

Thank you so much, this encourages and refreshes me!

LikeLike