I was afraid when my student loans were set for repayment on June 1, 2011. Throughout the years, I’ve researched and made my share of mistakes in my student loan debt journey. Here are a few resources and tips that have helped me along the way.

I was afraid when my student loans were set for repayment on June 1, 2011. Throughout the years, I’ve researched and made my share of mistakes in my student loan debt journey. Here are a few resources and tips that have helped me along the way.

1)Know who you owe and how much.

Visit www.nslds.ed.gov to get the name of your loan servicer and their contact information. Communicate with your loan servicers as soon as possible, missing payments can impact your ability to buy a house.

2) Split your monthly payment into bi-weekly payments.

This is a little hack I discovered homeowners use to reduce interest amount paid over the life of the loan.

Make sure that your payments are made before the due date. If you pay under the monthly amount, you risk accrual of interest and other penalties. Consult with your student loan servicer for more details.

The below tool allows you to see the impact of making biweekly payments. Click on the link below to view how my loan amount is impacted by making bi-weekly payments. Experiment with this calculator by entering your own loan amount and interest rate.

https://www.calcxml.com/calculators/should-i-convert-to-a-bi-weekly-payment-schedule?skn=#results

The standard student loan repayment term is 120 months or 10 years, you can edit this calculator to reflect when you expect to complete repayment. (1 year = 12 months)

3) Choose your major wisely.

Consider salaries for jobs within your major. Not every job will pay well for booksmarts and passion, so know your REALISTIC earning potential. For example, social workers don’t earn millions of dollars a year.

Using Finaid’s calculator, you can discover what minimum salary is needed to afford loan repayment. According to Finaid, I need to earn at least $117,807.27 annually to repay my debt comfortably. Honestly, not making anywhere near this salary minimum has caused for lots of sacrifice and struggle.

Review your minimum salary needed for repayment below.

http://www.finaid.org/calculators/loanpayments.phtml

4) Choose the repayment plan that works best for you.

www.studentloans.gov

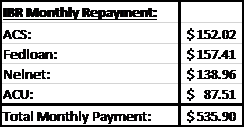

My loan servicers have calculated my updated monthly payments to be $45. The reduced monthly payment allows me some wiggle room if I ever fall on hard times.

However, $45 would not cover monthly accrued interest. Not only must you pay the interest, but you also want to pay down a sizeable amount of principal. Paying more than the minimum amount will effectively reduce your debt load and decrease the amount of time you are in debt.

Which leads us to the fifth point…

5) Make extra payments.

I currently make regular payments of $370 bi-weekly through money earned at my full-time job. Additional payments above the $370 bi-weekly amount are from my part-time job.

I have developed a strong hate for my student loans and try to throw as much money at them as possible. I refuse to have student loans when my kids start college.

6) Be Honest. Live below your means.

We all want to live in a certain area or drive a nice car. But at this time for me, the finer things in life aren’t worth the work required to obtain.

It gets difficult at times to tell friends and family members about my financial struggles, but I enjoy very strong relationships. Everyone won’t appreciate your honesty, get ready to develop thick skin.

7) Build a support system.

I’ve learned that you must simply ride the waves of life, as it is possible to feel alone in a room full of people. The key to life, in my opinion, is working to achieve full dependency on someone besides yourself. For me it’s my relationship with Jesus Christ and right now, I need some Jesus time.

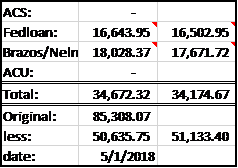

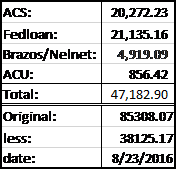

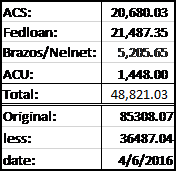

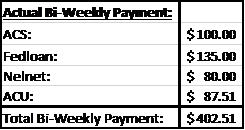

Below is an update on my student loan accounts. Until next time folks, be blessed and fight on!

I didn’t intend to write and post on a holiday break from work. However, it weighs heavy on me. Today, the United States commemorates the life and accomplishments of Dr. Martin Luther King Jr. He was a man who stood firmly for what he believed in, that we are all created equal by a holy and sovereign God. His dream was for a united America, not just for unity’s sake but under a righteous God.

I didn’t intend to write and post on a holiday break from work. However, it weighs heavy on me. Today, the United States commemorates the life and accomplishments of Dr. Martin Luther King Jr. He was a man who stood firmly for what he believed in, that we are all created equal by a holy and sovereign God. His dream was for a united America, not just for unity’s sake but under a righteous God.