Check out No Debt But Love’s student loan update for October featuring a special little helper.😄

No Debt But Love

😱😱😱Vacation in Hawaii with Sallie Mae😱😱😱

🙏Sending up prayers to those impacted by the tornado in Dallas.🙏

🏀🏀🏀October 2019 Student Loan Update | $14,275.07 Original Balance $85,308.07🏀🏀🏀

💰💰💰Why You Should Refinance Student Loan Debt💰💰💰

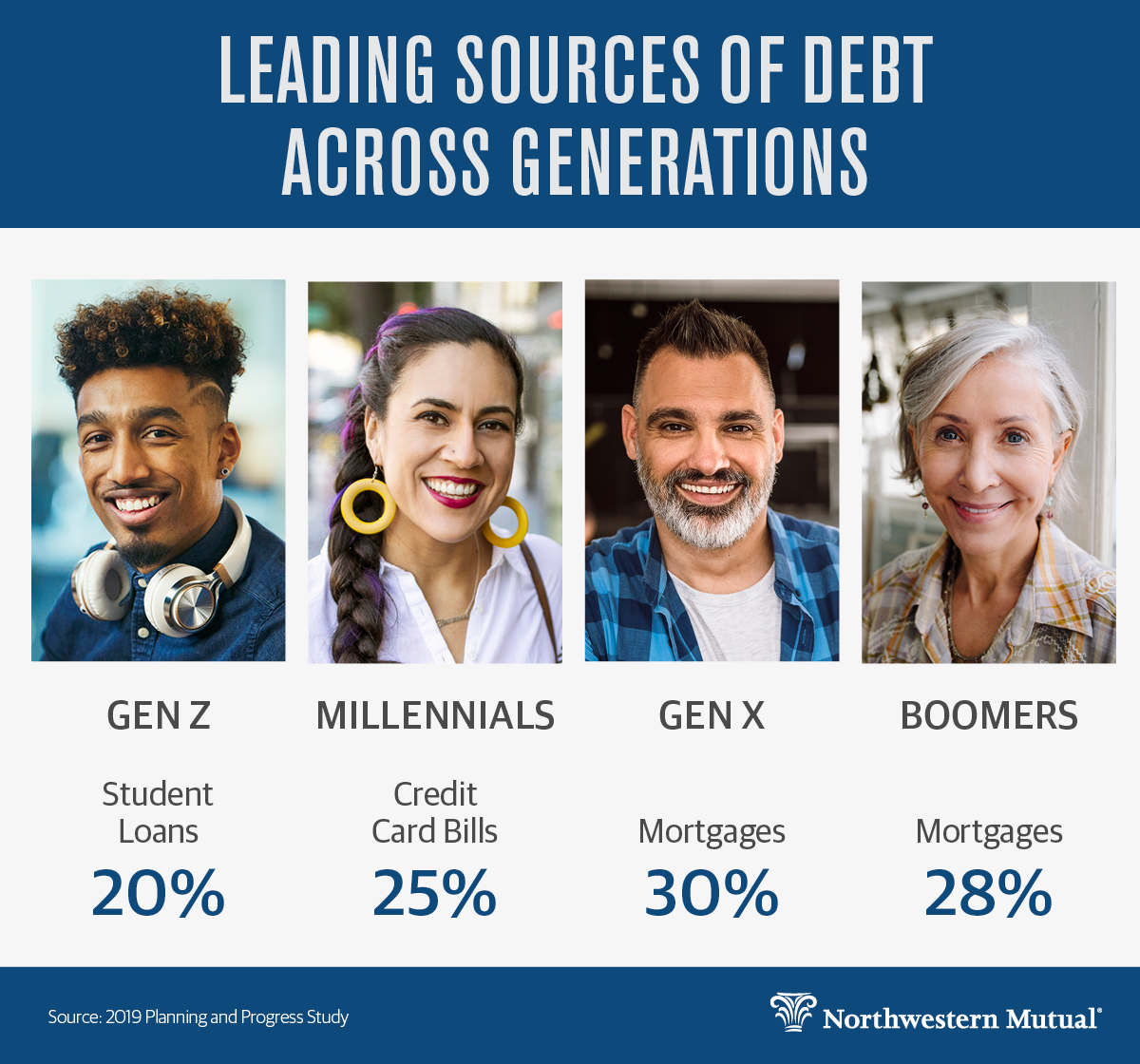

In The News: Millennials have an average of $28,000 in debt—and the biggest source isn’t student loans

September 20, 2019

By Megan Leonhardt, CNBC

It may seem like student loans and millennials are inextricably linked. But a new survey shows that education bills are not the leading source of debt among this generation.

Millennials (defined here as ages 23 to 38) have racked up an average of $27,900 in personal debt, excluding mortgages, according to Northwestern Mutual’s 2019 Planning & Progress Study. The findings are based on a survey conducted by The Harris Poll of over 2,000 U.S. adults.

The biggest source of debt? Credit card bills. And that’s a “troubling” trend, Chantel Bonneau, a financial advisor with Northwestern Mutual, tells CNBC Make It.

“One issue that a lot of millennials have is that they have not wanted to sacrifice their lifestyle, even though they have student loans or lower incomes,” Bonneau says. “That has left us in this spot where they’ve accumulated a significant amount of credit card debt.”

To Read More, Click Link Below:

https://www.cnbc.com/2019/09/18/student-loans-are-not-the-no-1-source-of-millennial-debt.html

In The News: Raising the Bar for Loan Forgiveness

September 16, 2019

By Andrew Kreighbaum, Inside Higher ED

In her first significant act as Education Secretary more than two years ago, Betsy DeVos said she planned to overhaul an Obama administration student loan rule designed to protect borrowers defrauded by their college.

Despite her efforts, the Obama borrower-defense regulations took effect last year. But on Friday DeVos capped off a two-year effort by issuing her own rule, which scales back loan forgiveness opportunities for student borrowers.

The new regulations significantly raise the bar for student borrowers seeking debt forgiveness based on claims they were defrauded by their colleges. They add a new three-year time limit for those borrowers to file claims, and each case will be considered individually, even if there is evidence of widespread misconduct at an institution.

Borrowers will also be asked to demonstrate they suffered financial harm from their college’s misconduct and that the college made deceptive statements with “knowledge of its false, misleading, or deceptive nature.”

The collapse of the Corinthian Colleges chain and subsequent flood of debt-relief claims prompted Education Department officials under the last administration to issue the 2016 borrower-defense rule.

Although the rule was a response to misconduct in the for-profit college sector, it applied to all Title IV institutions. And private nonprofit college groups had expressed concerns that their institutions could be on the hook for student claims even for unintentional mistakes in marketing materials. DeVos had made clear previously that she thought the regulations were too permissive, essentially offering borrowers the chance at “free money.”

“We believe this final rule corrects the wrongs of the 2016 rule through common sense and carefully crafted reforms that hold colleges and universities accountable and treat students and taxpayers fairly,” she said in a statement accompanying the rule.

Education Department officials said the new three-year time limit for claims aligns with record-retention requirements for colleges. They said the process will give institutions the opportunity to respond to claims and students the chance to elaborate on claims based on those responses.

The DeVos regulations will save the federal government about $11 billion over 10 years, the department estimates (the federal government shoulders the cost of loan discharge if it cannot recoup funds from the institutions themselves). Consumer advocates argue those savings are created by rigging the system against borrowers.

To Read More, Click Link Below:

🔨 🔨 🔨 Labor Day | September 2019 Student Loan Update | $15,006.89 Original Balance $85308.07 🔨 🔨 🔨

In The News: Families, Not Just Students, Feel The Weight Of The Student Loan Crisis

September 4, 2019

By Elissa Nadworny, NPR

For many college students settling into their dorms this month, the path to campus — and paying for college — started long ago. And it likely involved their families.

The pressure to send kids to college, coupled with the realities of tuition, has fundamentally changed the experience of being middle class in America, says Caitlin Zaloom, an anthropologist and associate professor at New York University. It’s changed the way that middle class parents raise their children, she adds, and shaped family dynamics along the way.

Zaloom interviewed dozens of families taking out student loans for her new book, Indebted: How Families Make College Work at Any Cost. She defines those families as middle class because they make too much to qualify for federal aid — but too little to pay the full cost of a degree at most colleges. For many, the burden of student debt raises big questions about what a degree is for.

This conversation has been edited for length and clarity.

How would you describe the world of student debt?

Families have really been transformed by debt, and really by the problem of dreaming about sending a kid to college and trying very hard to pay for it — oftentimes from the very earliest moments of a child’s life. I think what we don’t take account of, nearly enough, is what that experience is like — [what] the experience of trying to give a kid a shot by sending them [to] college means for most middle class families.That’s the thing that I think that we need to be focusing on.

You argue in the book that the idea of going to college is pervasive in American life.

It is pervasive. That message is coming at families from every direction: that being a success in America depends upon the ability to get into college, to get an education and to graduate. But that itself depends on the ability to pay, which thrusts us right into the paradox of it all — which is that on the one hand, young adults and the parents who support them have this very clear goal about getting a college education. On the other hand, that is going to cost them dearly.

Click On Link Below To Read More

In Pursuit Of More: $69,937.11 Paid, $15,370.96 Till Payoff

And we know that in all things God works for the good of those who love him, who have been called according to his purpose. -Romans 8:28

I Tried To Take It Back…

So often I am tempted to get angry, sulk, and take revenge because of a wrong someone has done to me. I run from discomfort, but what if you and I were meant to endure hardships? Never in a thousand years would I have imagined saying the following in a conversation, “Debt repayment and budgeting is not about managing your money, it’s about managing your heart”.

WHAT? I wish I could take those words back, as my wife grinned from ear to ear in acknowledgment of what implications that truly had on our current way of life. But it was too late.

I didn’t want to admit that despite my laser focus to repay my debt, at the end of the day, it was the process and not the details that carry eternal significance.

I didn’t want to admit that despite my laser focus to repay my debt, at the end of the day, it was the process and not the details that carry eternal significance.

Previously, I’d fantasize about receiving checks in the mail that could completely wipe out my debt. Sadly, the check never came; and the truth that I was alone in my debt journey hit me like a ton of bricks.

Before going to college, I saved every penny I had. My relationship with money as a child was not a healthy one–as I didn’t grow up with much. I knew money was needed to purchase things, but I also felt that having too much of it was wrong.

My Thoughts On Money

I think that money is a tool, and it doesn’t have any more power over you than you allow it to have.

Money is NOT inherently evil. The LOVE of money is the root of all evil. -1 Timothy 6:10. Love can be defined as an intense feeling of deep affection.

The emotion of love can influence us to accomplish heroic feats such as this father saving his daughter from a shark attack.

https://www.washingtonpost.com/sports/2019/06/04/paramedic-dad-punched-shark-five-times-save-his-daughter-who-lost-leg-attack/?noredirect=on

This man literally gave a shark the One Punch Man knuckle sandwich lunch special for FREE-99 lol. That shark will think twice before going after anything else besides marine life.

Risking It All

Or this strong fondness of something can destroy your life’s work. Take Bernie Madoff and Jefferey Epstein for instance, both men have been disgraced due to their misuse of things they enjoyed out of context.

Taking things out of the context from which they were meant to be enjoyed is dangerous. For one man, having enough money was never enough; for the other, seeking inappropriate affection.

I would like to leave you with a line from a song from an artist called Bizzle and an update on my student loans below.

Partial Lyrics from song by Bizzle “God Over Money”

If that same resource was made free to you

It would literally destroy what cash means to you

So how you risk your life for a paper dollar?

When as long as you have life you can make a dollar?

Student Loan Update

Until next time everyone! Stay strong… fight on… and have no debt but love! Peace and Blessings.

In The News: Americans are staying silent on student loan debt—and it’s not helping

August 19, 2019

By Megan Leonhardt, CNBC

When it comes to uncomfortable conversations, Americans would rather talk about pretty much anything else — politics, health issues, religion — than discuss their finances.

Yet the money topic Americans voted as most thorny is one that’s constantly in the news: student loans. Over a third of Americans say they see student loan debt as the biggest financial taboo, according to a Harris Poll of over 1,000 U.S. adults commissioned by TD Ameritrade.

A similar survey conducted by the MIT AgeLab and sponsored by TIAA found that 40% of respondents reported they never talk to their family about their student loans. In fact, over half said their families know “nothing” or “very little” about their debt.

Yet you’re far from unique if you’re swimming in student loan debt. Americans have amassed $1.5 trillion in student loan debt, with one in four Americans carrying a balance. And both the prevalence and the effect of student loans is widely studied: the Fed found that 20% of the homeownership decline among millennials (ages 24 to 32) can be attributed to this debt. Other surveys have found that student loan debt is forcing millennials to put off other major life milestones, such as getting married and starting families.

Democratic 2020 presidential candidates are even making student loan debt solutions a core component of their campaigns — promising everything from better refinancing options to introducing more debt forgiveness programs to wiping it out completely.

So why aren’t people talking about their student loans around the dinner table or with friends over drinks? It’s personal, experts say. “Student loan debt may be pervasive and a constant topic in the media and in the political arena, but it’s still debt,” Erin Lowry, author of Broke Millennial Takes On Investing, tells CNBC Make It. “People are fundamentally uncomfortable talking about debt because it’s easy to assume another person is going to pass judgement on your choices.”

And boy do they.

Click On Link Below To Read More: