I am finally “under the hill”–I now owe less than $50,000 in student loans! Bring out the bubbly!

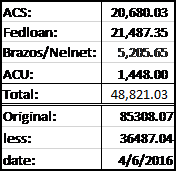

Here’s a snapshot of my current loan accounts:

If you were to meet me 5 years and told me where I would be today, I would either deem you a lunatic or a liar. Because 5 years ago, my loan balance was nothing to celebrate…

Holiday Blues 2011:

My heart felt heavy with guilt and shame as I drove home from work one week before Christmas in 2011. The holidays are some of the worst times to feel blue, especially due to job loss. It was my third time being dismissed from work in two years. I walked into my apartment without a word after cheerful greetings and a kiss from my wife.

Know How Much You Owe:

Thoughts rushed in at once, “Who gets fired a week before Christmas? How are you going to pay rent?” And the scary one, “How are you going to make your student loan payments?” I can happily say it has been 4 years, 8 months since I have started this journey. What helped reduce my student loan debt was knowing how much I owed. It is possible to track student loan amounts using the National Student Loan Data System’s website.

Taxes & Payment Plans:

If Benjamin Franklin were alive today, his famous quote would read, “In this world nothing can be said to be certain, except death, taxes, and student loans”. Fortunately, for today’s college graduates, Income Driven Repayment plans exist to make repayment easier.

The federal government offers four repayment plans known as: Repaye, Paye, IBR and ICR. Under my current repayment plan, the first three years of interest was waived, and all payments went to principal. To remain in one of these repayment programs, however, you must submit tax information annually (the processing of which can (surprise!) be incredibly inefficient, but I’ll save that episode for another time). Thankfully, this documentation can be submitted electronically through Studentloans.gov.

Being enrolled in an “income-based” program made repayment possible during times of unemployment. In addition, many are eligible to receive up to a $2,500 tax deduction. This interest deduction has saved my wife and I lots of money, especially since she is now a full-time student.

For more details about the federal government’s income-driven repayment plans, click here.

The End In Sight:

I constantly review my repayment schedule, and in doing so, keep myself motivated as to the finite nature of this “student loan phase” of life. One of the most concrete ways to accomplish this is through using a repayment calculator. A simple, yet effective calculator can be found through FinAid.org. The website can print a repayment schedule based on your loan amount, interest rate, and loan term. It is a tailored picture you can always revise to help envision your expected payoff date, and gives you the ability to play around with your payment budget and see the effects.

I hope this information has been helpful in providing motivation, goals, and vision. You, too, can make progress in your repayment journey by:

1) Knowing what you owe,

2) Taking advantage of tax and repayment options, and

3) Seeing the end.

Feel free to post any specific questions, or additional advice you have gained on your journey, below!

Until next time, continue the fight, friends.